New York City, 20 Jul 2020: The global Aircraft Fuel Systems Market size is expected to reach USD 7.50 billion by 2026 according to a new study by Polaris Market Research. Aircraft fuel systems are designed to provide uninterrupted and uncontaminated free fuel regardless of the aircraft’s attitude. As fuel load take a significant portion of airliner’s weight, a sufficiently strong airframe is designed in a way to control fuel loads and shifts in weight. This is an essential system which pumps, manages, and delivers jet fuel to the propulsion system and auxiliary power unit (APU). The implementation and functional characteristics play a critical role in design, certification, and operational aspects of both military and commercial jets. These systems directly affect the performance of an airliner as compared to any other airplane system.

Companies such as Collins Aerospace, Eaton, GKN Aerospace Services Limited, Honeywell International Inc., Meggitt PLC, PARKER HANNIFIN CORP, Safran, Triumph Group Inc., and Woodward Inc., are some of the major vendors operating in this industry.

|

| Request For Sample |

Aircraft fuel systems are designed to provide uninterrupted and uncontaminated free fuel regardless of the aircraft’s attitude. As fuel load take a significant portion of airliner’s weight, a sufficiently strong airframe is designed in a way to control fuel loads and shifts in weight. This is an essential system which pumps, manages, and delivers jet fuel to the propulsion system and auxiliary power unit (APU). The implementation and functional characteristics play a critical role in design, certification, and operational aspects of both military and commercial jets. These systems directly affect the performance of an airliner as compared to any other airplane system.

Globally, flights generated about 915 million tonnes of CO2 in 2019 which is equivalent of 2% of all human induced CO2 emissions (42 billion tonnes). Aviation sector is responsible for 12% of CO2 emissions in transportation industry as compared to 74% emitted by road transport. Government and Federal Organizations are trying to regulate tough protocols for airplane OEMs and fuel system manufacturers in order to reduce the carbon emissions. An airplane fuel system consists of mainly storage tanks, valves, pumps, and metering & monitoring devices which are designed under strict Title 14 of the code of Federal Regulations guidelines. To meet the FAA requirements, the manufacturers design the systems which are free from vapor lock when using the jet-fuel at critical temperature. The tanks are separated from personnel compartments of the aircrafts by fume-proof and fire-proof enclosures which are vented and drained to the exterior of the airplane. The components of this system are bonded and grounded in order to drain off static charge.

Furthermore, increasing global airliner fleet, increasing commercial & regional airplane production & deliveries, growing revenue passenger kilometers, growing demand of lightweight components for achieving higher fuel efficiency & save costs, rising demand for fuel efficient & lightweight fuel systems are some for the major factors aiding in the growth of global industry.

Among airplane type, the market is segmented into commercial, military, and UAV. Commercial airliners are expected to be the largest market in 2019, owing to increasing production rates of the commercial airliner models such as B737, B787, A320, A350XWB, C919, A320 Neo, B737 Max, B777x, and A330 Neo. This segment is also propelled by rising commercial jet deliveries to support growing passenger traffic pushed by rising per capita income. Moreover, introduction of new generation fuel-efficient airliner models such as B737Max and B787 Dreamliner is another major factor aiding in the growth for the industry globally.

Among technology type, the market is segmented into pump feed, fuel injection, and gravity feed. In 2019, pump feed was estimated to be the largest market for fuel systems globally. This technology is majorly used on commercial and military jets as these are mid and low-wing airplanes with wing location not above the engines. The technology uses fuel-pumps to deliver the fuel from the tanks to engines.

Among component type, the market is segmented into pumps & valves, fuel tank, piping, gauging, inerting systems, and others. In 2019, gauging was estimated to be the most dominant component type followed by pumps & valves. Gauging is basically an instrument with sensing unit in the tank & indicator in the dashboard which is used to indicate and monitor amount of fuel in a tank. Pumps are used for transferring the fuel from the tanks to the carburetor whereas valves regulates & controls the flow by opening and closing or by obstructing the various fuel passage directions.

Among engine type, the market is segmented into jet engine, helicopter engine, turboprop engine, and UAV engine. In 2019, jet engine was estimated to be the most dominant engine type, according to Polaris Market Research. Jet engine basically powers the commercial airplane, regional planes, business jets, and military aircrafts. Increasing production rates of commercial airplane models such as A320, B787, B737, and Bombardier C series is one of the major factors aiding in the growth for jet engine segment and thereby driving the industry.

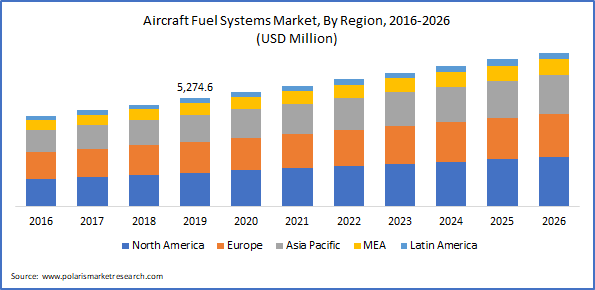

Among region, North America is expected to remain the largest region for aircraft fuel-systems globally as this region is the manufacturing capital of aerospace & defense industry due to large presence of aircraft OEMs, component manufacturers, fuel system vendors, distributors, and raw material suppliers. Moreover, presence of largest airplane fleet in the region is another major factor aiding the growth in this region.

In case, any of your pain points areas are not covered in the current scope of this report, Request for Customization here : https://www.polarismarketresearch.com/industry-analysis/aircraft-fuel-systems-market/speak-to-analyst

No comments:

Post a Comment